Issue #3: December 2019/January 2020

Issue #3: December 2019/January 2020

China in the Arctic: Part 1

This month it’s an appropriately wintry edition (at least in the Northern Hemisphere), as I take a look at Chinese activities in the Arctic. There’s plenty to get into on this topic, so I’ll be splitting it into two parts. This month I’ll concentrate on Russia, a state which, whether seen as competitor or collaborator, is central to China’s Arctic ambitions. Next month I’ll take a look at some of the other polar states where China’s presence is growing.

But first...a shameless plug.

My book In China’s Wake has just been released by Columbia University Press. It tells the story of how in the early part of the 21st century, Chinese demand drove a boom in commodity prices which in turn created space for the emergence of a variety of new development models across resource-rich states (I cover 15 countries, from Argentina to Zambia). Find out more here: https://cup.columbia.edu/book/in-chinas-wake/9780231187978 and get 30% off by using the promo code ‘CUP30’.

Ok, back to the Arctic….

CHINA, THE US, AND THE ARCTIC

On 20th December Donald Trump signed the US National Defense Authorization Act into law, with a price tag of $738bn (roughly equivalent to the entire annual economic output of Turkey). Though Trump’s pet Space Force project and the removal of several anti-war amendments attracted coverage, one of the less commented upon parts of the Act is a call for an investigation into China’s investment activities in Arctic states.

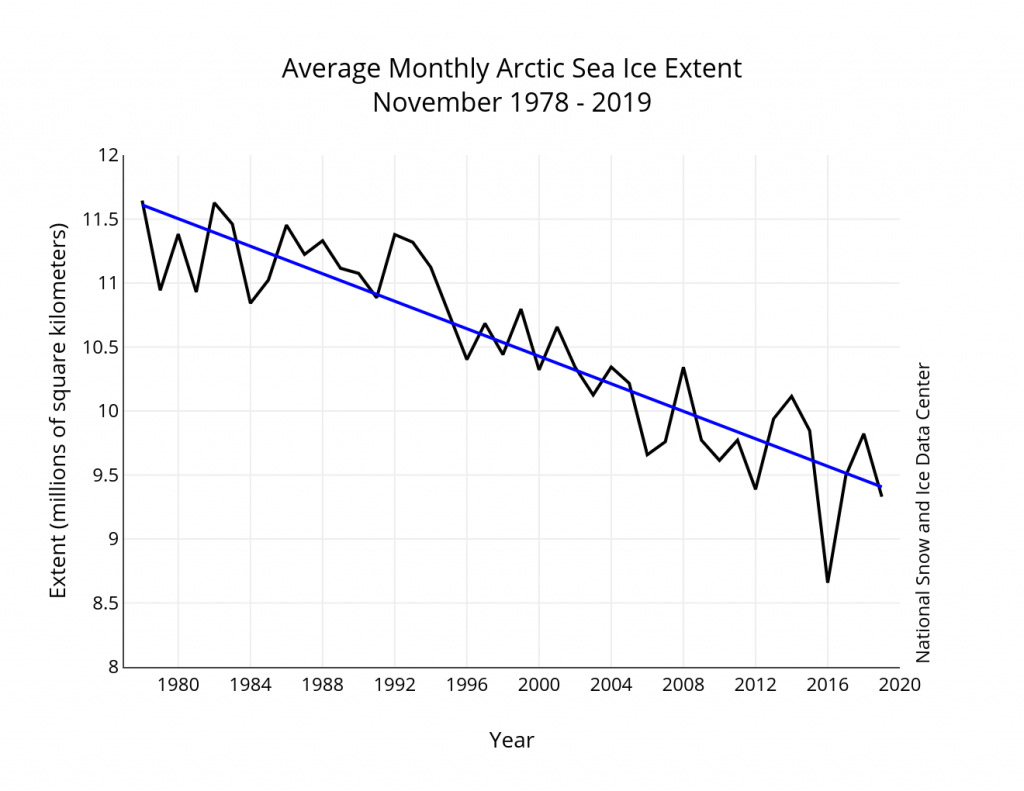

As climate change warms the far north, retreating sea ice cover is increasingly opening the Arctic Circle to shipping, research, tourism, military activity and resource extraction (in a sad irony, especially oil and gas). As good as the reasons may be for limiting many of these activities near the poles (and something similar is unfolding in the Antarctic, too), a melting Arctic is fast becoming a new frontier for economic expansion (and strategic competition). Chinese authorities are keenly aware of the region’s importance, not least because of its implications for the world’s largest trading and shipping nation as the ice melts and makes polar sea routes more viable. This interest isn’t new- Xi Xinping spoke of an intention to become a ‘polar great power’ back in 2014- but it continues to develop, with the ‘polar silk road’ becoming an official part of the Belt and Road Initiative in 2018. Along with various scientific and economic projects, China’s growing involvement in the High North is now significant enough to prompt a reaction from Washington.

November Arctic sea ice extent for 1979 to 2019 shows a decline of 5 percent per decade.

Source: NSIDC

With its most northerly point (in Heilongjiang) lying at the same latitude as the Netherlands and British Columbia, the PRC has nevertheless sought to present itself as a legitimate stakeholder in the North, calling itself a ‘near-Arctic’ state. However, with no territorial claims in the region, Chinese strategy has been to stress multilateralism as a means of preventing the far North from becoming the exclusive domain of countries whose sovereignty extends into the Arctic Circle. Those states- Russia, Canada, the US, Finland, Sweden, Norway, Iceland and Denmark via Greenland- comprise the full members of the Arctic Council, a forum that also includes ‘participants’ representing the region’s indigenous groups. China is an official observer at the Council (a status which has also been granted to the likes of India, Germany, France and the UK), but in recent years has been stepping up its bilateral engagements with several of the full members.

Source: Public domain

It is here that US concerns lie, prompting the demand for an official report on Chinese investments in the region. In part this reflects the usual worries about Chinese infrastructure projects serving as a backdoor for potential later military use, something which has already prompted the cancellation of a major Chinese port project on Sweden’s west coast. It seems virtually impossible that any of the Arctic states would allow the People’s Liberation Army to operate on their territory, even if there are instances where Chinese civilian ventures may also have possible military or intelligence applications. Beyond security aspects, however, questions similar to those which have dogged the BRI around the world have also followed it to the Pole. First, the potential political and economic leverage over other sovereign states which China might gain via its loans and investments. Second, in a region with 4 million inhabitants (including 40 indigenous groups) and a particularly vulnerable ecosystem, what are the social and environmental results likely to be? There is plenty to talk about here in relation to most of the different Arctic states- and in terms of non-Chinese projects too.

CNA Analysis and Solutions (a non-profit closely tied to the American foreign policy establishment) produced a report in late 2017 on investment in the Arctic that seems to have informed the US Administration’s current thinking. The report claims that Chinese polar investments are already substantial, equivalent to 6% of GDP in Iceland and 12% in Greenland, with nearly $200 billion going to Russia. Coming up with accurate numbers on Chinese financial flows overseas is notoriously difficult (as I’ve discussed previously) and the figures here are both hazily defined (they roll up everything from loans to stock purchases, joint ventures and credit lines under the banner of ‘investment’) and probably inflated (for example, they include China Non-Ferrous’ involvement in the planned Citronen Fjord zinc mine in Greenland, financing which will only materialise if zinc prices rise enough to make the project worth taking forward). But it doesn’t take much reading between the lines to see that the report’s call for new regulatory controls on Arctic investment (and a new US-led Arctic Development Bank) is an effort to pre-emptively limit China’s reach into the area. These ideas have been taken up in the NDAA, with the call to investigate Chinese investments also asking for a study into the feasibility of an Arctic Development Bank. This is all framed in terms of making sure future polar investments are socially and environmentally responsible, surely a tough case to make about any new fossil fuel projects, especially in the Arctic wilderness (drilling in remote parts of Alaska has been permitted by Trump, of course, and would be encouraged under the report’s proposals).

THE NORTHEAST PASSAGE

The Northeast Passage (with the portion inside Russian waters known as the Northern Sea Route) runs from the Bering Sea, north through the Bering Strait and then west along the northern coast of Russia before finally reaching the Barents and then Norwegian seas. Shipping has regularly traversed the passage since the 1930s, although the hazards involved make it too risky and expensive to be used as a major cargo route, at least for the moment. As the ice recedes and thins, though, navigation will become easier, with current projections of ice free Summer waters from around 2040. Since travelling this way shaves off around a quarter of the distance between Shanghai and Rotterdam from the usual trip via the Suez Canal, it is easy to see why interest in the NE Passage has picked up in recent years. For China, a viable Northern route would also present a means of avoiding the strategic pinch point of the Straits of Malacca, a goal which informs both the Polar Silk Road strategy and other projects such as the overland road and pipeline corridor from Gwadar on the Arabian Sea to the Pakistan-Xinjiang border.

Since the NE Passage crosses warmer waters and has better search and rescue infrastructure, it looks a better bet for shipping than the Northwest Passage (through the Canadian Arctic)- and certainly than the transpolar route which may become viable in mid- to late-century. That said, the NE Passage is likely to remain expensive (often requiring ice-classing of ships and/or icebreaker escort) and unreliable (unpredictable ice floes can delay journeys significantly) for some time yet. That combined with shallow waters which make it impassable for the largest cargo vessels mean its use as a route for just-in-time shipping will probably continue to be a limited one. Where we are likely to see serious expansion, however, is in the use of the NE passage as a route for shipping oil and liquid natural gas, the development of which underpins all of Russia’s plans for the Arctic.

WESTERN SIBERIA

Climate change is happening faster in Siberia than almost anywhere else. On 5 January Russia published a climate change adaptation plan, which warns of incoming dangers (melting permafrost, floods, wildfires and disease) but seeks to harness ‘positive’ effects, not least of which is the growing accessibility of new resource deposits in the Arctic, especially natural gas.

Zapolyarnoye gas field, Yamalo-Nenets Autonomous Okrug, Russia

Source: government.ru

Russia’s economy is heavily dependent on oil and gas exports- and government officials have claimed that the country’s oil production could soon go into decline unless more is done to find and exploit new deposits. While there are almost definitely major untapped reserves in the Russian Arctic, there are technological challenges involved that mean help from western oil firms would likely be needed for extraction, difficult to arrange while Russia is under US and EU sanctions. Instead, activity has concentrated on liquid natural gas (LNG). Most natural gas is transported via a pipeline (like the new Russia-China ‘Power of Siberia’ pipeline). But LNG- whereby gas is supercooled to become a liquid, reducing its volume to just 0.2% of the original gas, making it possible to transport via ship- is becoming more important, especially for Russia.

In late 2018 Russian energy firm Novatek finished work on Yamal LNG, a $27bn LNG plant and port at Sabetta, on the east shore of the Gulf of Ob, which opens onto the Kara Sea. Lying 520km north of the Arctic Circle, it is now the most northerly industrial facility in the world. Novatek has plans for another massive LNG plant on the Gydan Peninsula across the Gulf of Ob from Sabetta (this one costing $21bn). Both projects have been impacted by US sanctions, which have effectively made it impossible to raise money in dollars. This has left an opening which Chinese banks and firms have been happy to fill, to the tune of $12bn in the case of Yamal LNG (perhaps surprisingly, French and Japanese firms are also involved, despite the sanctions).

This matters for China because of its growing demand for natural gas imports. Air pollution is a serious issue for the PRC, with the potential to cause social unrest. As a result, in 2017 the government stepped up efforts to convert coal burning to gas across Northern China. The programme ran into problems, including shortages of gas which left many without heating. Efforts to boost a slowing economy mean that the coal to gas drive has been relaxed this Winter, but China is still going to be the main source of demand growth for gas over the coming years. From the Chinese perspective, reliable supplies of gas from Russia would help the PRC avoid too much dependence on alternative sources (mainly Qatar, the US and Australia), most of which are more vulnerable to sanctions and protectionism (indeed, any resolution to the US-China trade war will probably mean China committing to import more American LNG). Meanwhile, major Chinese investments in the Russian Arctic (China National Petroleum Corporation and the Silk Road Fund own 30% of Yamal-LNG between them) give China some leverage over the Arctic LNG industry and help strengthen PRC claims to be a legitimate stakeholder in the region. From the Russian perspective, this is about opening up a supply route lying almost entirely within Russian waters, lessening dependence on European export markets and maintaining Russia’s position as a major energy power.

Whether the LNG ventures will push Russia and China closer together in a geostrategic sense remains to be seen. And Russia’s LNG push may well slow down or speed up as fluctuating gas prices make new projects more or less attractive. But the US sanctions on Russia and trade war with China have certainly made Russian-Chinese economic cooperation more mutually beneficial, especially in the Arctic. If that trend continues, it may even eventually have an impact on the global dominance of the US dollar. As for the Arctic, there is something deeply contradictory about a drive for cleaner air in China being met by new fossil fuel projects in the Siberian Tundra, where a changing climate is already making life harder for the local Nenets people.